Court Memo Details $350K+ Probate Valuation Gap Linked to Affordable Housing Board Member

Court Memo Details $350K Probate Valuation Gap

Linked to City Affordable Housing Board Leadership.

Pro Se Tenants Continue to Face Exploitative Tactics When They Seek Justice

An Analysis of How Court Procedures, Counsel Conduct, and Information Asymmetry

Perpetuate Housing Injustice Even After Litigation Begins

Defense AI Disclosure Motion: Pre-AI Case History Disproves Competence Suspicion

Lawyers Question Pro Se Competence, Miss Basic Docket Search Showing Strategic Legal Arguments Pre-AI Against Their Own Client

Why Systems Thinking and Strategic Thought Leadership in Housing Justice?

As systems thinker Russell Ackoff said, "A bad system will beat a good person every time."

The Altman Files: When Public Trust Meets Private Extraction

Court Filing Reveals City Affordable Housing Commissioner Linked to 95% Asset Devaluation, "Flash Transfers," and Displacement of 5-Year Tenants in Good Standing.

Discovery Is Not a Word Game: Motion to Determine Sufficiency of Defendants’ RFA Response

When “vague and ambiguous” becomes a strategy, Requests for Admission stop narrowing issues and start hiding them. Motion seeks court intervention after defendants deployed coordinated "vague and ambiguous" boilerplate to avoid clean admissions.

Meridian Residential Group’s Privacy Invasion: Unauthorized Family Images Published Across 25+ Platforms

Meridian Residential Group published and distributed photos of plaintiffs, their older family dog in diapers, and their belongings on at least 25 websites for months without the tenants' knowledge or consent.

When Two Firms Coordinate to Hide Evidence Before a Regulatory Deadline

Coordinated Obstruction, Unconsentable Conflicts, and Witness Tampering in Real Time

The Health Crisis Filings: Tenant Harm Weaponized Through Defense Gaslighting

Defense Claims 'Threats' After Criminal Complaint Filed, Gaslighting Pattern Produces PCL-5 Score of 76/80, Co-Plaintiff Intervenes as ADA Accommodations Requested

Mitigation of Damages with Strategic Thought Leadership Demo

Proving to a Jury the Value of what was lost through re-launching it Using this Case as a Leverage Point for Paradigm Change in Housing:

A Real-Time Demonstration of the Power of the Destroyed Platform.

Experience it for yourself: Test with Interactive Links Below.

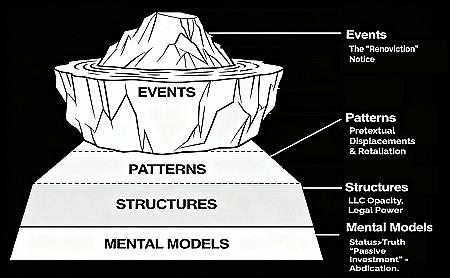

Housing Justice Audit Report (Draft)

A scathing condemnation of the "Unconscious Abdication" Mental Model behind "Passive Investing" and the viscous cycles of harm it causes in the Charleston, SC Housing and Housing Justice System.

And a clear plan for true positive change with an alternate model called Conscious Co-Stewardship (CCS)

Self-Represented Tenant is Actually a Consultant Studying the System

Shedding the "Vulnerable Tenant" disguise, the Systems Analyst Asks the Court to Confront Institutional Betrayal, and Sets the Tone for addressing Charleston’s Housing Crisis

Settlement Is Permanently Off the Table with Trial Commitment

Plaintiffs Irrevocably Withdraw All Settlement Offers and Demand Jury Trial After Documenting Six Conditions of Institutional Failure - SC Supreme Court Exhibits Attached

SC Supreme Court Demands Answers in Rare Tenant Victory in Housing Crisis-Ravaged Charleston.

Fourteen days to undo 189: How a pro se petition exposed a 33:1 motion processing disparity and forced the SC Supreme Court to bypass the entire appellate ladder, directing the Ninth Circuit Court of Common Pleas to answer for months of silence.

Filing to Judge Wheeler: "Save Us From Charleston's Coming Captured System Collapse"

Plaintiffs seek forensic audit, Temporary Restraining Order, and SLED referrals as an 86-page Notice exposes how Charleston's legal, housing, and media ecosystems protected a false narrative until SC Supreme Court intervention.

The SC Supreme Court Missing Writ

How a Four-Day Documentary Test Exposed Selective Docket Suppression at South Carolina's Highest Court.

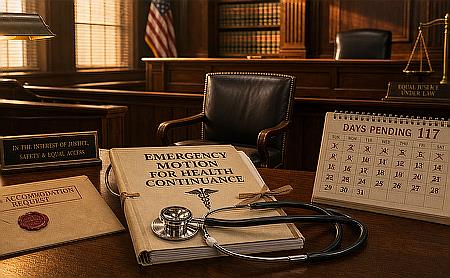

The Emergency Health Motion They Denied

South Carolina's judge selection process enables vulnerability to capture. How a denied emergency continuance and related, ignored-for-4-months ADA accommodations motion exposed the human cost of such capture through the impact on a disabled pro se litigant.

Mayor Cogswell, the Altman Appointee, and Closing the Courthouse Door

The rental house at the center of this tenant-exploitation lawsuit financially benefits Jonathan S. Altman, who advises Mayor Cogswell on affordable housing from the Homeownership Initiative Committee.

On March 27, 2026, Plaintiffs put the Mayor on notice. The same week, court staff branded a disabled pro se litigant's all-parties safety filing "ex parte and not allowed," while the same litigant's formal ADA accommodation request sat unanswered for nearly two months - and defense counsel's remote-hearing request, one of the ADA accommodations requested January 20, 2026, and never granted, was promptly accommodated.